Source: Supplied

A growing percentage of card transactions now include payment surcharges passed onto customers, Australian fintech Zeller says, as some SMEs consider new ways to counteract surging operating costs.

Zeller released its inaugural Small Business Resilience Report on Monday, detailing the ways inflation and changing consumer habits are rippling through the sector.

Two out of five surveyed businesses called the rising cost of supplies and materials their primary concern, with one in three chiefly worried about a downturn in consumer spending.

The report touches on how businesses are striving to make up that gap, either by increasing the price of goods and services, or increasing sales volumes.

But the report also investigates the role of card transaction surcharges in recouping some, or all, of the costs of handling debit and credit payments.

Card providers and payment platforms often take a small cut of each transaction processed via debit or credit card to pay for the cost of providing those services to the merchant.

The Australian Competition and Consumer Commission (ACCC) allows merchants to pass those costs onto customers, so long as the surcharge does not exceed the transaction fee faced by the business and relates only to the kind of payment made by the customer.

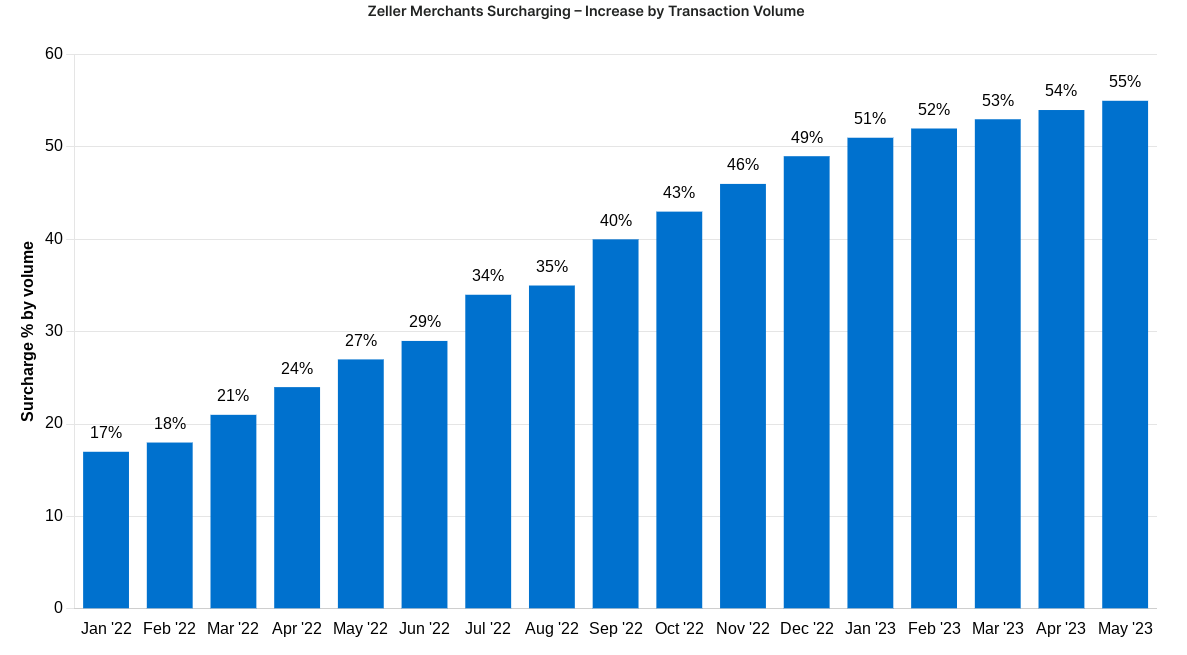

The volume of transactions processed through Zeller’s EFTPOS Terminal units which feature a surcharge has surged in the past year, the new report states.

Some 27% of Zeller transactions by volume included a surcharge in May 2022, jumping to 55% in May this year.

By contrast, just 17% included a surcharge in January 2022.

Source: Zeller

What types of businesses are applying a surcharge?

Joshua McNicol, Zeller’s head of growth, said the growth of surcharging remains relatively consistent among sectors that have historically adopted the practice, like transport, home and maintenance, travel, hospitality, and the professional services industries.

“We’re still not seeing as much penetration in some of those newer verticals like retail or things like that, where it’s just not as commonplace,” he said.

The key factor is whether customers in those sectors are willing to accept an extra surcharge, he added.

“We find that it’s definitely not the majority of businesses who have adopted this practice,” McNicol said.

“While the percentage of the volume of transactions which are applying this may have increased, particularly in this very tough economic period where businesses are looking to survive and try to thrive, I think that businesses are applying them when they know their customers and their competitive landscape.”

However, the Zeller report itself does hint at how some more traditional retailers are passing on card transaction fees to their customers.

Matt Bisaro of Sydney florist Floral Craftsman told the fintech he faced some opposition from customers when his business first applied a surcharge.

“Now you can add on that surcharge and no one thinks about it, ’cause everyone’s doing it,” he said.

Indeed, big businesses have long adopted surcharging into their practices, with McNicol singling out ALDI as a prime example.

While McNicol says small businesses should carefully consider how customers in their niche will react to an extra cost at the checkout, Zeller itself has long speculated the big business approach to surcharging may filter down to smaller competitors.

“As more and more businesses opt to surcharge, it’s likely more smaller merchants will take a leaf out of bigger merchants’ books and pass the cost of accepting cashless payments on to customers,” the company said in February.

How else can I reduce transaction costs?

Beyond levelling a card payment surcharge on customers, there are other avenues small businesses can consider to keep transaction costs down.

Least-cost routing (LCR) allows merchants to select the payment processing pathway which applies the lowest transaction fees each time a customer uses a contactless card payment.

This can allow merchants to route contactless debit purchases through the EFTPOS system, instead of the framework offered by the card provider, which may charge higher transaction fees to the business itself.

The ACCC also permits restaurants, cafes, and hotels are free to charge weekend and public holiday surcharges (unrelated to card payment fees) to counteract heightened penalty rates paid to staff.

However, businesses should carefully balance those surcharges against their customers’ willingness to stomach further price hikes, with several businesses making headlines in recent weeks for their decision to pass those costs on to consumers.

Although the vast majority of in-person payments made in Australia are now made through contactless card transactions or mobile wallets, cash acceptance still remains a simple way to avoid merchant fees.

Maintaining a physical cash register can maintain payment options for customers still set on physical currency while allowing a business to sidestep card fees.

ABOUT THE AUTHOR

Handpicked for you

Small businesses brace for Australia Post price hike on July 3, with some expecting to pay $5 more per parcel

COMMENTS

SmartCompany is committed to hosting lively discussions. Help us keep the conversation useful, interesting and welcoming. We aim to publish comments quickly in the interest of promoting robust conversation, but we’re a small team and we deploy filters to protect against legal risk. Occasionally your comment may be held up while it is being reviewed, but we’re working as fast as we can to keep the conversation rolling.

The SmartCompany comment section is members-only content. Please subscribe to leave a comment.

The SmartCompany comment section is members-only content. Please login to leave a comment.